How finmid built 10-minute payouts

What happens in those 10 minutes?

Up to the point before a merchant accepts the offer, we have assessed them anonymously. Acceptance changes that. The merchant agrees to share their data, and before the payout is triggered, we have one final obligation: confirm who is actually getting paid.

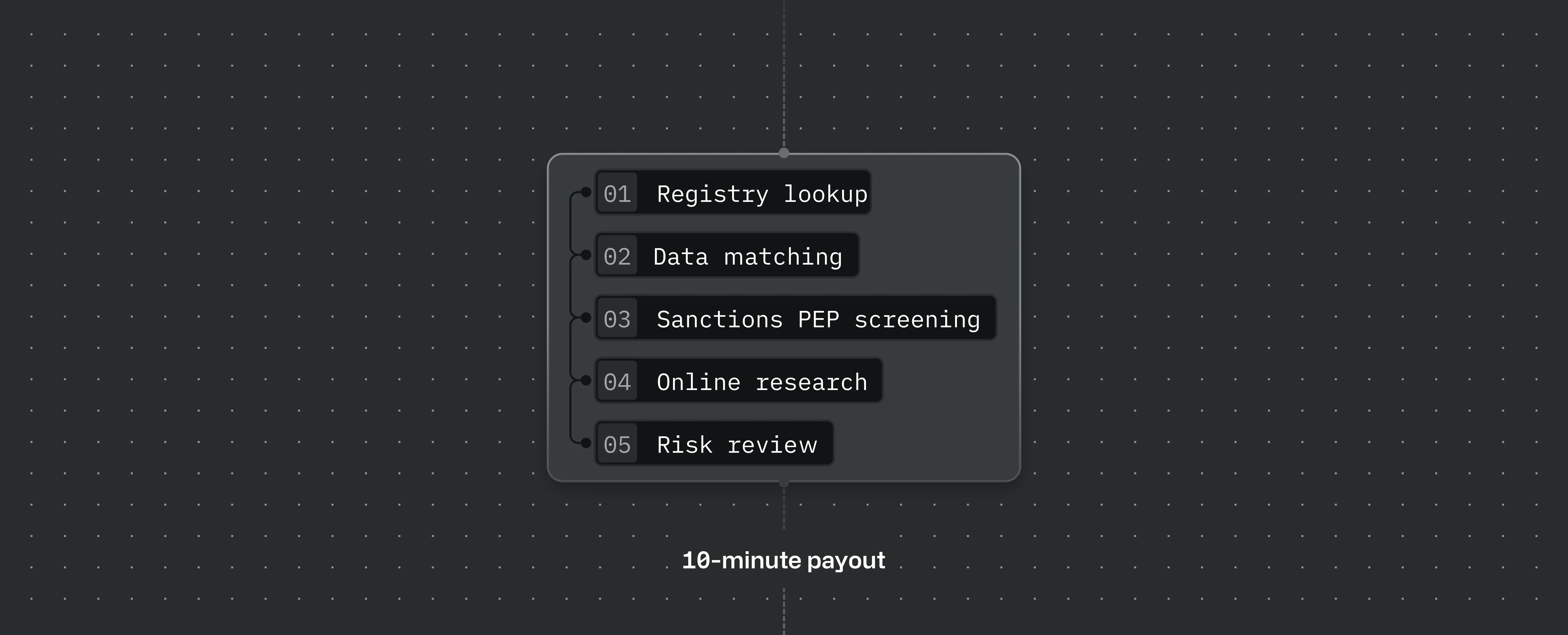

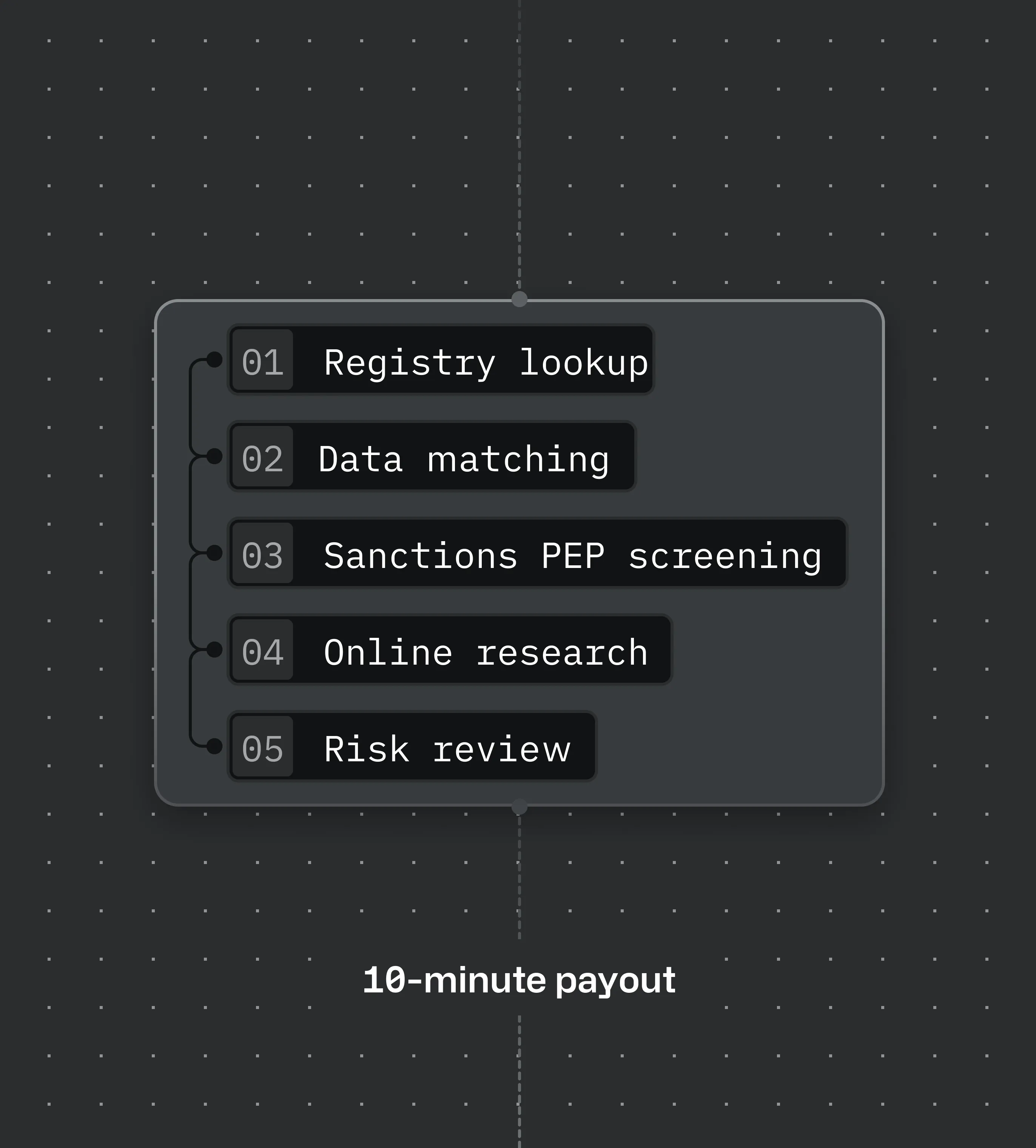

That process happens in five steps:

-

1.

We look up the merchant’s record in official business registries to confirm the business actually exists in public records.

-

2.

We match the merchant’s data the platform shares with us against what we found in the registry, to confirm the two align.

-

3.

We screen the merchant against global sanctions and PEP lists to ensure they are not sanctioned entities.

-

4.

We research the merchant online to build a fuller picture of who they are.

-

5.

We conduct a final risk review, applying the specific rules mandated by our risk team.

The top three improvements that made 10-minute payouts possible

The journey to 10-minute payouts was not a single breakthrough. It was a series of deliberate bets on automation. Here are the three that had most impact.

The most impactful was automating business online research. This step used to be entirely manual: an operations analyst would investigate each merchant one by one, a process that took 30 minutes on average.

We replaced that with agentic workflows built on tools like Gemini or OpenAI. The workflow runs in three stages:

-

1.

A first agent scrapes the web for anything it can find on the business: fraud allegations, legal issues, health violations, but also positive signals like expansion news or strong ratings.

-

2.

A second agent then checks whether each result actually refers to the business we are evaluating, rather than another company that happens to share its name.

-

3.

A third agent takes everything surfaced by the first two and classifies the merchant into a risk bucket according to our rules.

The result: automation above 90%, and average completion time down from 30 minutes to 2.

The second most impactful change was automating data matching. Traditional approaches like exact string matching or basic fuzzy logic could only automate 4% of cases. The issue is that real-world data is messy in ways algorithms cannot anticipate. "Smith & Co Ltd" on a platform and "Smith and Company Limited" in a public registry are obviously the same business to a human. To a rules-based system, they are a mismatch. As a result, the vast majority of cases ended up in a manual review queue.

We rebuilt this using large language model-based matching. Rather than comparing strings, the model reasons about whether two representations refer to the same underlying entity, accounting for name variations, address abbreviations, entity structures, and language differences. Automation jumped from 4% to 70% overnight. What had been one of our biggest operational bottlenecks became our fastest step.

The third improvement was automating business registry lookup. European data infrastructure is a patchwork of national systems and third-party providers with different coverage and reliability. The breakthrough was building our system to route each lookup to the best available source for that specific market, rather than defaulting to a single provider. That alone compressed this step to 30 seconds.

The integration that makes 10 minutes possible

If a business successfully passes all five steps, funds are paid out within 10 minutes of acceptance. It is an unparalleled value proposition for platforms and for the merchants they serve.

One important prerequisite: the 10-minute window only holds when finmid and the platform have an embedded data-sharing setup in place.

That integration is what allows merchant data to flow to us in real time the moment they accept the offer. Without it, data is forwarded manually, and minutes become hours.

Why this matters

Many embedded lending programmes are optimised for launch. That is the wrong finish line.

We built 10-minute payouts because we have seen where programmes break. The real test is the day edge cases start compounding faster than your team can handle them.

Embedded lending is an operating system. At finmid, we build for what happens after you say yes.

Curious to see how embedded lending could work for your platform? Book a demo.

finmid is the embedded lending infrastructure powering platform growth. With its API, finmid enables platforms to launch tailored financing products for their business customers at scale. Across industries, borders, and business models, finmid drives revenue, improves retention, and fuels core business growth. finmid is trusted by Europe’s most ambitious platforms, including Wolt, Delivery Hero, Just Eat Takeaway, Glovo, and FREENOW. Learn more at finmid.com.